The idea of this article will be to explain how the system works, but also to shed some light on what you can get and what are your options. We will try to answer to following questions: Where does that money go? What’s the difference between EU and non-EU? Is it different if I’m employed or freelance? Can I get my contributions back if I go “home”? How much will I get at retirement?

How does it work?

So you’re an expat living and working in the Czech Republic for some time now! You may have noticed something on your tax declaration that is being sent to social security every month! Well, the Czech pension system is divided in 3 pillars.

The one that you are participating in is the 1st pillar, the public pension. This pillar is MANDATORY. You can’t avoid it, unless you’re a diplomat! As soon as you’re a tax resident here, your employer or you will need to make these payments.

The money goes to a government institution called the CSSZ (or social security). If you’re employed, your employer will send it there for you every month, but if you’re a freelancer, you should be making monthly “deposits” and at the end of the year “settle” the difference (if you’ve made a lot more money than anticipated, you must pay more, and vice versa). The higher your income, the higher payments you will make to the CSSZ.

Great! So this money is mine then? Unfortunately, not. The funds accumulated are then redistributed to people who are currently retired. So basically, the older retired people living in Czech Republic now are being paid from our wages… And therefore, logic abides, that when you will retire, you should receive your share from the youngsters working at that time!

This doesn’t seem fair for expats!

If you’re an expat and thinking that you will not retire here, so why should you participate? You don’t have a choice. It’s the law. Just like, expats in your home country are participating in your home country pension scheme. If you leave the country before retirement, you also can’t get your participation back. Why? The social security already gave it away!

What’s next, then?

Since you are participating, it gives you the right for a public pension at retirement. There are 2 main conditions:

- Must be 65 years old

- Must have participated in the social security for 35 years

If you are meeting these conditions you are eligible for old age retirement pension.

How much will I get?

Some expats believe that they will receive less than Czech people, just because they’re foreigners. This is FALSE. The amount you will get is based on your income over the 35-year period and your overall participation.

So, since expats get on average higher income than Czech people, the average expat pension should be higher. However… the current average pension in the Czech republic is ~12,000 CZK per month. On top of that, 2/3 of the population is receiving less than that! The CSSZ is using a formula to calculate the amount you should be receiving for your retirement.

But, by taking a closer look, you can notice that there’s an increasing penalty that grows bigger with higher incomes! Which basically means that the higher your income the more you pay into the system, but the less you will get in terms of percentage of your income!!!

Why is it so unfair? One word: Solidarity. The government feels that since you were blessed enough to have such a nice income during your lifetime, you should be able to fend for yourself, and social security will protect the less fortunate than you.

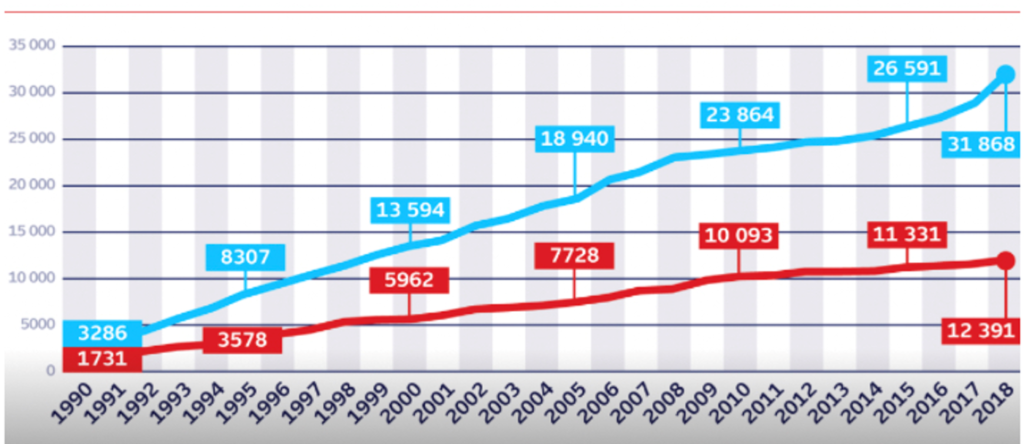

In the above graph, the blue line represents the average Czech income between 1990 & 2018. The red line represents the average pension between 1990 & 2018. In 1990, the pension was about ~50% of the income. In 2018 it is around ~30%. This gap will continue to widen in the future.

A word of advice… Whatever you do, never rely fully on the government for your future retirement!

Frequently Asked Questions

I am from the EU and heard about the global EU pension sharing scheme. What about it?

It is a bit complex, but it exists. Let’s say you work 10 years in Czech Republic and then go to your home EU country to live, work and eventually retire. The 10 years that you have worked here are not lost and will be calculated towards your overall retirement. There are the conditions of CR and your home country that will apply to receive a full pension. On top of this, these conditions are subject to change and will very most likely increase in the future.

Example: Work 10 years in Prague and then 20 years in Paris. Overall, you have 30 years of work in the EU, which unfortunately is not enough to receive the Czech part of the pension. You would need 25 years of work in Paris, to get to the 35 years requested by CR to get your Czech part. Now the other tricky part is that the French conditions applies as well, which is 40 years of work! So, to receive full complete pension from both countries you would need to work 40 years in all of EU combined to receive it without penalties!

I am non-EU, what happens to me?

If you work here for a few years, then decide to go back to a non-EU country to live, work and retire, you are facing a riskier outcome. You must first check if your country has a special agreement with the CR in terms of pension exchange. If it does, then the similar logic to EU citizens applies. If it does not, then you probably won’t be able to claim your pension if you do not fulfill the conditions.

Is there a difference between employees and freelancers?

Both face the same situation in terms of the conditions and how the system works. The only difference will be in terms of their contributions. Basically, as a freelancer it is possible to declare expenses when doing taxes, and technically if the government thinks that you’re broke, they won’t ask much from you for your pension contributions. However, this means that your public pension will be extremely low and beware since this technique can block you from getting a mortgage as well!