Let’s face it, Financial Planning doesn’t make us jump out of bed in the morning 🙂 Typically, it’s something we know we should do but we tend to kick it further down our “to do” list to next week, after the summer holidays, in the New Year, next pay raise ….. but what’s the cost of not doing anything now? Let’s take a look.

Let’s face it, Financial Planning doesn’t make us jump out of bed in the morning 🙂 Typically, it’s something we know we should do but we tend to kick it further down our “to do” list to next week, after the summer holidays, in the New Year, next pay raise ….. but what’s the cost of not doing anything now? Let’s take a look.

What enables us to live our lives as we do? Money, right? Our income keeps a roof over our heads, puts food on our table, clothes on our back. It lets us enjoy all the fun things, going to nice restaurants, amazing holidays, nights out with friends. It helps us through the tough times, if we get sick or have a family emergency, it pays for medical help or flights back home. So, if our income does all this and more, why don’t we look after it?

We tend to take our regular, reliable income for granted and don’t think about the consequences of no longer having this, but like everything in life, all good things must come to an end, so what’s the cost of NOT protecting our income and planning for our future?

1/ Our retirement:

Close your eyes for a second. Imagine you wake up tomorrow and you are retired (I can see you all smiling now at the thought :-)) Where will you be? What does your day look like? Travelling? Lazy breakfasts overlooking the sea? Spending time with the family? Spending time on a new project or a hobby you’ve always wanted to do but never had the time for? Sounds great? So, what will you live off?

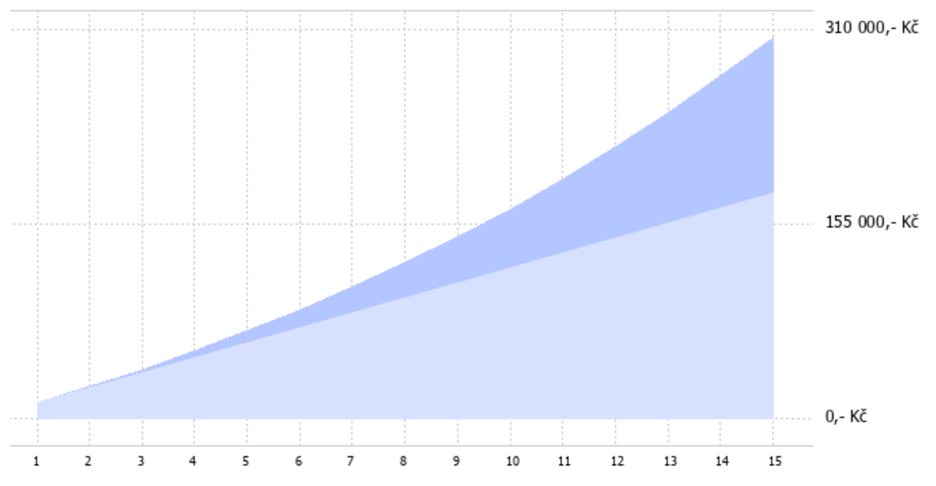

Imagine now, that throughout your working life you’ve not planned for this day because the state will give you a pension. In reality, the state may provide a pension, however, this realistically will be peanuts! In Czech Republic, the monthly state pension paid out today is around CZK 12,000, however, with current demographics, people are living longer and there is less of a working population, so fast forward another 30 years and this same state pension will be lucky to be around CZK 3,000 per month in today’s money (see pension article for more details). So back to the question, what will you live on?

Does this mean you have to keep working for another 5 or 10 years? Or does it mean you have to struggle and count every penny spent, every day of your retirement? It doesn’t paint a pretty picture, but unfortunately, it’s reality for many people who didn’t plan ahead in time. The good news, however, is that you CAN make the choice to plan for your retirement now, plus the longer you have to save for this, the easier it is on your pocket 🙂

New pensions survey: Nearly half of Europeans not saving for retirement

“43% of European citizens are not saving anything privately for their retirements… “

(Source: https://www.insuranceeurope.eu/new-pensions-survey-nearly-half-europeans-not-saving-retirement)